Loan Performance Insights Report Highlights: April 2021

- The nation’s overall delinquency rate was 4.7% in April.

- All but one state logged an annual decrease in the overall delinquency rate.

In April 2021, 4.7% of home mortgages were in some stage of delinquency (30 days or more past due, including those in foreclosure)[1], which was the first year-over-year decrease and the lowest overall delinquency rate since March 2020 according to the latest CoreLogic Loan Performance Insights Report. The 1.4 percentage point decrease in the delinquency rate from April 2020 marked a turning point for mortgage performance and was enabled by an employment and income recovery that helped homeowners remain or return to “current” mortgage payment status.

Overall Delinquency Rates

The share of mortgages that were 30 to 59 days past due — considered early-stage delinquencies — was 1% in April 2021, down sharply from a post-pandemic high of 4.2% in April 2020. The share of mortgages 60 to 89 days past due was 0.3% in April 2021, down from 0.7% in April 2020 and down from a high of 2.8% in May 2020.

The serious delinquency rate — defined as 90 days or more past due, including loans in foreclosure — was 3.3% in April, roughly three times that of a year earlier, but down from a recent high of 4.3% in August 2020 and from 3.5% in March 2021. The CARES Act provides relief to mortgage holders and has worked to keep delinquencies from progressing to foreclosure and therefore the foreclosure inventory rate — the share of mortgages in some stage of the foreclosure process — remained low at 0.3% in April 2021, unchanged from April 2020. The decrease in the serious delinquency rate from the August high and increases in home equity as prices continued to increase in 2021 lessen the likelihood of a foreclosure wave later in the year when homeowners emerge from forbearance.

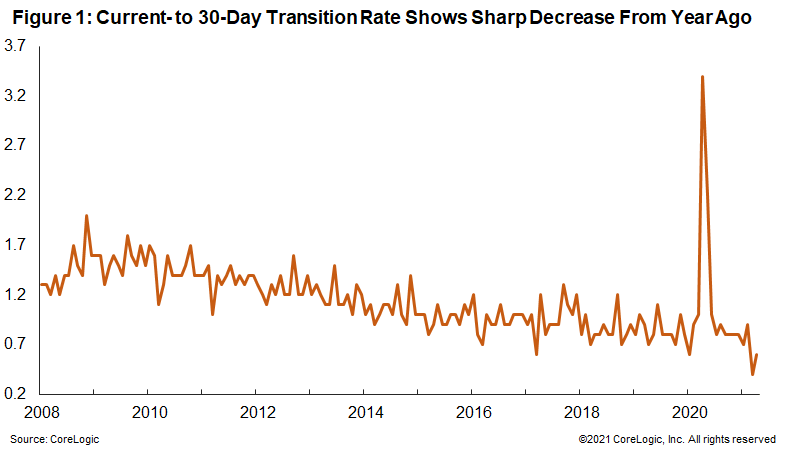

Stage of Delinquency: Rate of Transition

In addition to delinquency rates, CoreLogic tracks the rate at which mortgages transition from one stage of delinquency to the next, such as going from current to 30 days past due (Figure 1).

The share of mortgages that transitioned from current to 30 days past due was 0.6% in April 2021 — a sharp decrease from the peak of 3.4% in April 2020. Low transition rates indicate that while the rate of mortgages in any stage of delinquency remained elevated, fewer borrowers slipped into delinquency than early in the recession.

State and Metro Level Delinquencies

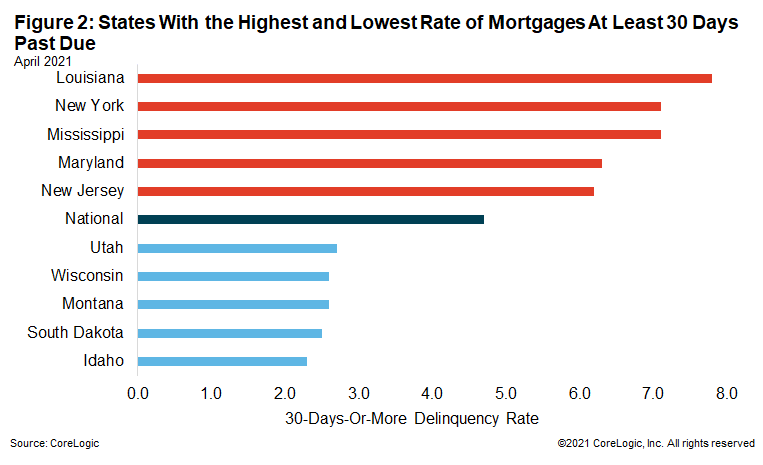

Figure 2 shows the states with the highest and lowest share of mortgages 30 days or more delinquent. In April 2021, that rate was highest in Louisiana at 7.8% and lowest in Idaho at 2.3%. All but one U.S. state posted annual decreases in their overall delinquency rate in April 2021. While Wyoming showed a small increase of 0.1 percentage points, the overall delinquency rate in that state was 3.8%, which was down from a post-pandemic peak of 4.9% in September 2020.

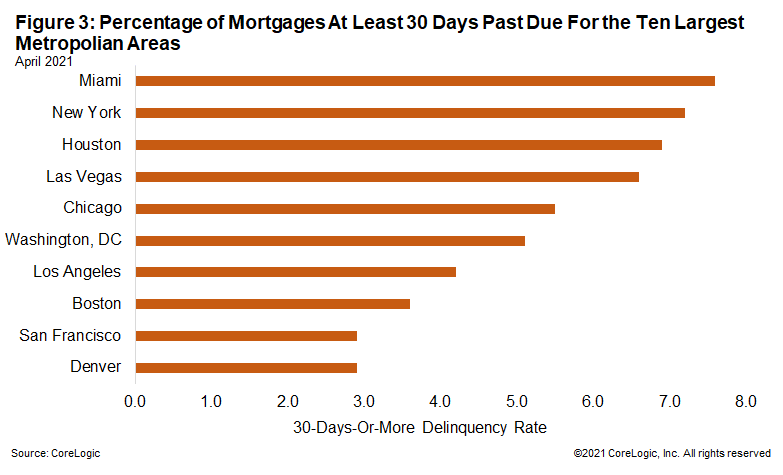

Figure 3 shows the 30-plus-day past-due rate for April 2021 for 10 large metropolitan areas.[2] Miami had the highest rate at 7.6% and Denver and San Francisco tied for the lowest rate at 2.9%. Miami’s rate decreased 3.9 percentage points from a year earlier. Outside of the largest 10, all but eight metros recorded a decrease in the overall delinquency rate, with the largest increases coming from metros with oil industry job losses. Odessa, Texas, had an annual increase in the overall delinquency rate of 2.4 percentage points, and Midland, Texas, had an annual increase of 2.3 percentage points.

Mortgage delinquencies fell from a year-ago for the first time since the pandemic, marking a turning point in mortgage performance. While the serious delinquency rate was elevated compared with the pre-pandemic period, early delinquencies were low in April. Continued improvements in the economy and job market this year will help borrowers remain current on their payments when forbearance is lifted later this year. For more housing trends and data, visit the CoreLogic Intelligence Blog at corelogic.com/intelligence.

© 2021 CoreLogic, Inc. All rights reserved.

[1] Data in this report is provided by TrueStandings Servicing. https://www.corelogic.com/products/truestandings-servicing.aspx. The CARES Act provided forbearance for borrowers with federally backed mortgage loans who were economically impacted by the pandemic. Borrowers in a forbearance program who have missed a mortgage payment are included in the CoreLogic delinquency statistics, even if the loan servicer has not reported the loan as delinquent to credit repositories.

[2] Metropolitan areas used in this report are the ten most populous Metropolitan Statistical Areas. The report uses Metropolitan Divisions where available.